Hey there, future homeowner! If you're diving into the world of mortgages, you’ve come to the right place. Mortgage rates today can be a game-changer when it comes to buying your dream home. Whether you're a first-time buyer or a seasoned property owner looking to refinance, understanding mortgage rates is crucial. Let’s break it down in a way that makes sense, so you can make the best financial decision for your future.

You’ve probably heard the term "mortgage rates" thrown around in real estate conversations, but what does it really mean? Simply put, mortgage rates today determine how much interest you’ll pay on the loan you take out to buy a house. These rates fluctuate daily based on various economic factors, and they directly impact your monthly payments. Knowing the current trends can save you thousands of dollars in the long run.

Before we dive deeper, let’s set the stage. The housing market is hot right now, and mortgage rates today are a key player in this game. Whether you're looking to lock in a fixed rate or go for an adjustable one, having the right information is key. So, grab a coffee, get comfy, and let’s explore everything you need to know about mortgage rates today.

Read also:Prmovies Download Movie Your Ultimate Guide To Streaming And Downloading Movies

Table of Contents

- What Are Mortgage Rates?

- Factors Affecting Mortgage Rates Today

- Fixed vs Adjustable Mortgage Rates

- Current Market Trends in Mortgage Rates

- How to Get the Best Mortgage Rate

- Common Mistakes to Avoid

- Loan Types and Options

- Refinancing Options

- Calculating Your Mortgage Payments

- Final Thoughts

What Are Mortgage Rates?

Alright, let’s start with the basics. Mortgage rates today refer to the interest rate charged by lenders on the money you borrow to buy a home. It’s essentially the cost of borrowing, and it’s expressed as a percentage. For example, if you’re getting a mortgage with a 4% rate, that means you’ll pay 4% of the loan amount in interest annually.

Now, here’s the thing: mortgage rates aren’t static. They change daily based on market conditions, economic indicators, and even global events. So, keeping an eye on these rates is essential if you’re planning to buy a house or refinance an existing mortgage.

Why Do Mortgage Rates Matter?

Mortgage rates today can significantly impact your financial future. A lower rate means smaller monthly payments and less interest paid over the life of the loan. On the flip side, higher rates can make homeownership more expensive. That’s why it’s crucial to understand how rates work and what affects them.

Factors Affecting Mortgage Rates Today

So, what makes mortgage rates today go up or down? There are several factors at play, and understanding them can help you time your home purchase or refinance decision better.

Economic Conditions

The state of the economy plays a big role in determining mortgage rates. When the economy is strong, rates tend to rise because there’s more demand for loans. Conversely, during economic downturns, rates often drop to encourage borrowing and spending.

Federal Reserve Policies

The Federal Reserve influences mortgage rates through its monetary policies. While the Fed doesn’t directly set mortgage rates, its decisions on interest rates can have a ripple effect on the housing market.

Read also:Girl Dies From Trampoline Punishment A Tragic Reminder Of Parental Discipline Gone Wrong

Inflation

Inflation is another key factor. When inflation rises, lenders often increase mortgage rates to compensate for the decreased purchasing power of money over time. It’s like a balancing act between lenders and borrowers.

Fixed vs Adjustable Mortgage Rates

When it comes to mortgage rates today, you have two main options: fixed-rate and adjustable-rate mortgages (ARMs). Let’s break them down.

Fixed-Rate Mortgages

With a fixed-rate mortgage, your interest rate stays the same for the entire term of the loan. This means your monthly payments remain predictable, which is great for budgeting. Most fixed-rate mortgages come with terms of 15 or 30 years.

Adjustable-Rate Mortgages (ARMs)

On the other hand, ARMs have interest rates that can change over time. They usually start with a lower introductory rate, which is fixed for a set period (e.g., 5 or 7 years). After that, the rate adjusts based on market conditions. ARMs can be risky but might save you money if you plan to sell or refinance before the rate adjusts.

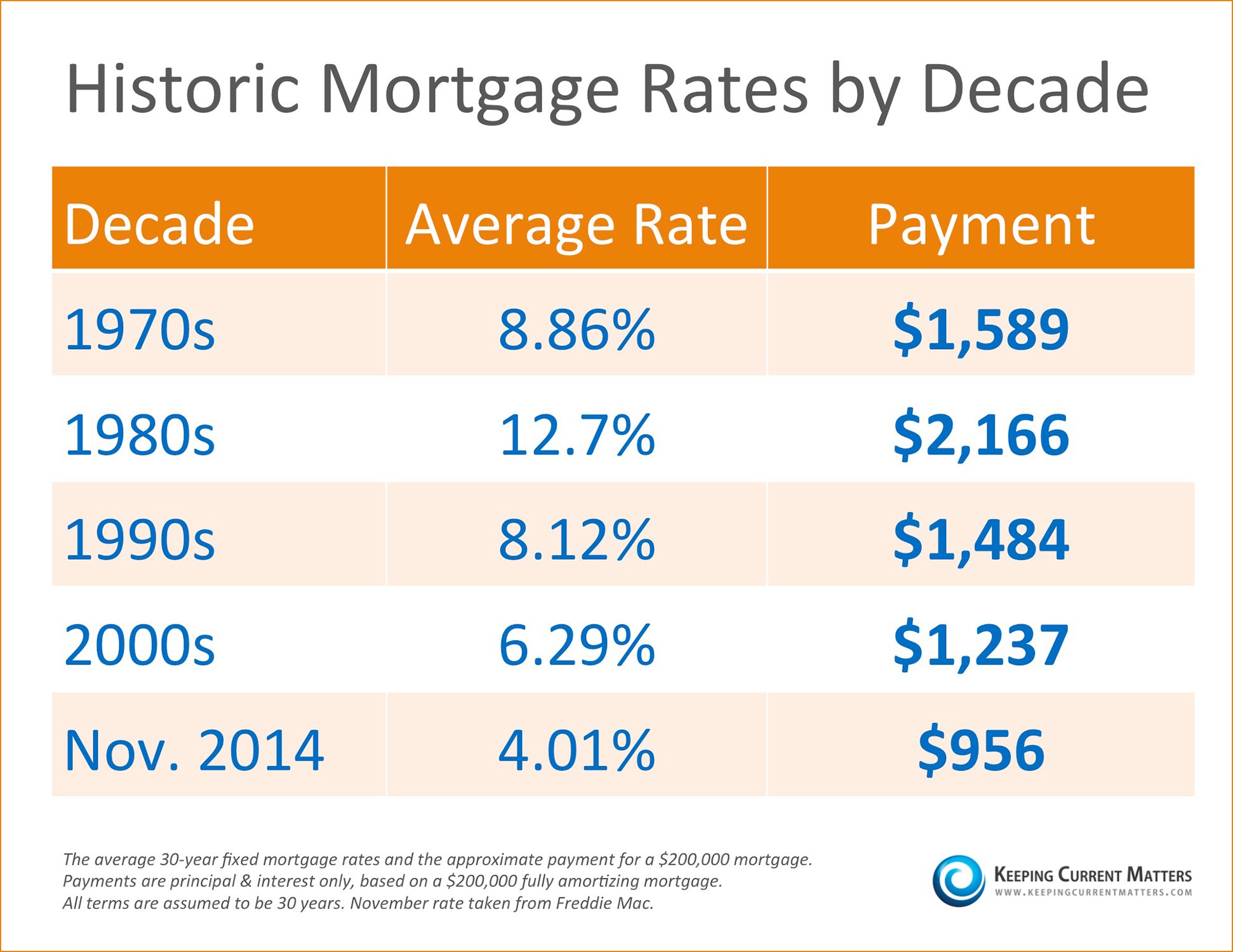

Current Market Trends in Mortgage Rates

As of now, mortgage rates today are showing some interesting trends. The housing market is still competitive, and rates are hovering around historical averages. However, there are signs of potential changes on the horizon.

Experts predict that rates might rise slightly in the coming months due to inflation and economic growth. That said, locking in a good rate now could be a smart move if you’re ready to buy or refinance.

How to Get the Best Mortgage Rate

Getting the best mortgage rate today requires some strategy. Here are a few tips to help you secure the lowest rate possible:

- Improve your credit score: A higher credit score can qualify you for better rates.

- Shop around: Compare offers from multiple lenders to find the best deal.

- Make a larger down payment: Putting down more money upfront can reduce your interest rate.

- Consider points: Paying points upfront can lower your rate over the life of the loan.

Common Mistakes to Avoid

When dealing with mortgage rates today, it’s easy to make mistakes that could cost you money. Here are a few pitfalls to watch out for:

- Not comparing lenders: Don’t settle for the first offer you receive. Shop around to find the best rate.

- Ignoring fees: Some lenders may offer lower rates but charge higher fees, so be sure to compare the total cost.

- Not locking in a rate: If rates are favorable, consider locking in your rate to protect against future increases.

Loan Types and Options

There are various types of loans available, each with its own set of mortgage rates today. Here’s a quick rundown:

Conventional Loans

These are standard loans offered by private lenders. They typically require good credit and a down payment of at least 3%.

FHA Loans

FHA loans are backed by the Federal Housing Administration and are ideal for first-time buyers or those with lower credit scores. They often come with lower down payment requirements.

VA Loans

Available to eligible veterans and service members, VA loans offer competitive rates and no down payment requirement.

Refinancing Options

If you already own a home, refinancing can be a great way to take advantage of lower mortgage rates today. By refinancing, you can reduce your monthly payments, shorten your loan term, or even cash out equity.

However, it’s important to weigh the costs and benefits before refinancing. Make sure the savings outweigh the fees associated with the process.

Calculating Your Mortgage Payments

Understanding how to calculate your mortgage payments can help you plan your budget. Here’s a simple formula:

Mortgage Payment = Principal + Interest + Taxes + Insurance

There are also plenty of online mortgage calculators that can do the math for you. Just input your loan amount, interest rate, and term to get an estimate of your monthly payment.

Final Thoughts

Mortgage rates today play a critical role in the homebuying process. Whether you’re a first-time buyer or looking to refinance, understanding rates and how they work is key to making smart financial decisions.

Remember, the housing market is dynamic, and rates can change rapidly. Stay informed, shop around, and don’t hesitate to consult with a trusted mortgage professional. With the right approach, you can secure a great rate and make homeownership more affordable.

So, what are you waiting for? Start exploring your options and take the first step toward your dream home. And hey, if you found this guide helpful, drop a comment or share it with a friend who’s also in the market. Let’s make homeownership a little less stressful, one mortgage rate at a time!